The EU compliance platform for AML-regulated firms

From onboarding to continuous monitoring - Meo helps EU firms meet their AML, KYC and KYB obligations with audit-ready confidence, ready for the AMLR single rulebook taking effect 10 July 2027.

Onboarding that converts

Client-owned & reusable data profiles

Real-time monitoring

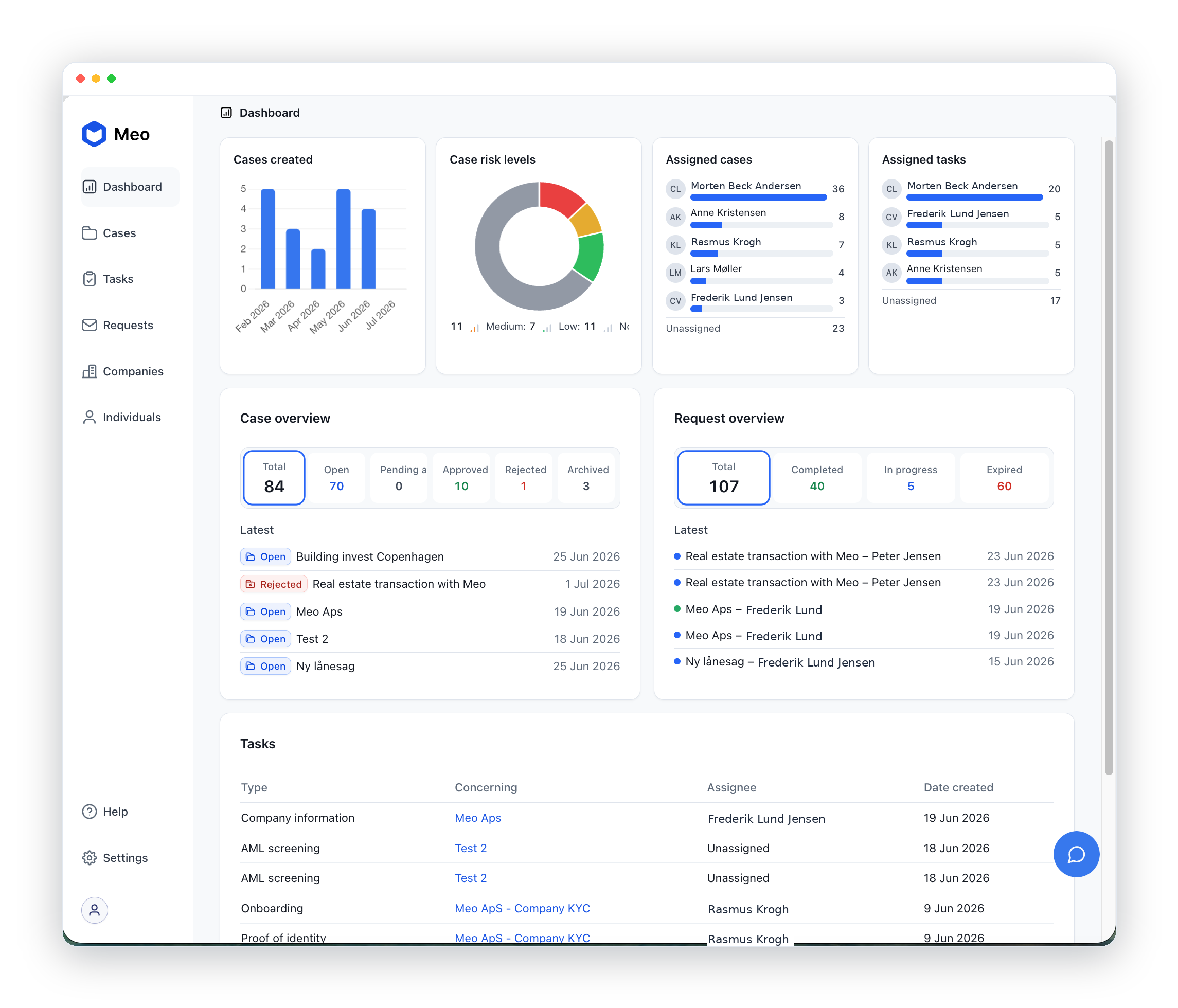

One platform for continuous AML compliance

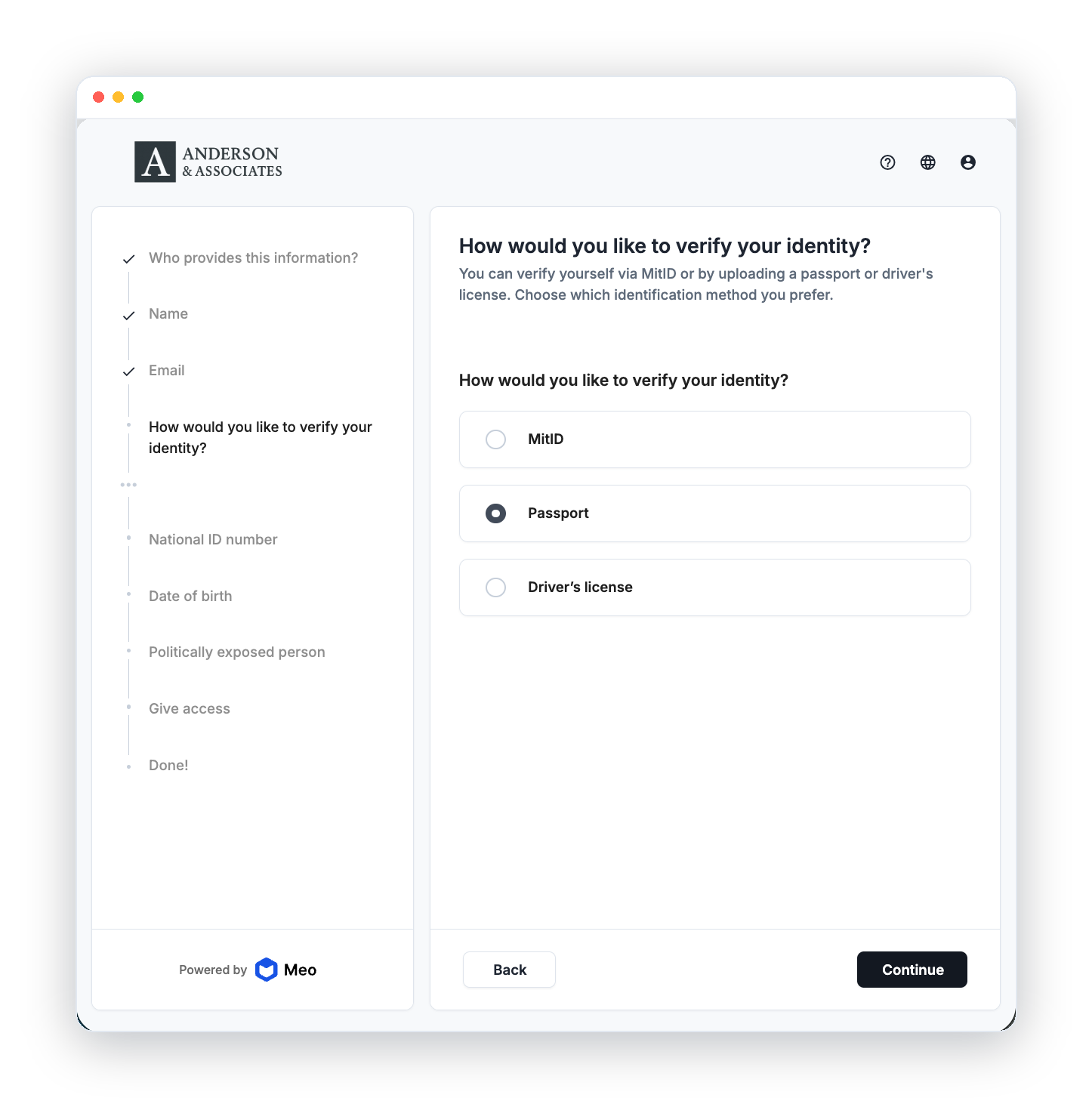

Client onboarding under your own brand

- Branded flows

Your logo, your colours, your domain. Clients complete onboarding in an experience that carries your firm's identity throughout. - Identity verification build in

National electronic ID (eID), passport or driver's license - clients verify directly in the flow, no separate tools or manual document handling. - Data confirmation, not collection

Existing client data is prepopulated, so returning clients verify rather than retype. - Prepopulated flows

Clients can receive their known data prefilled and simply confirm it, instead of entering everything from scratch.

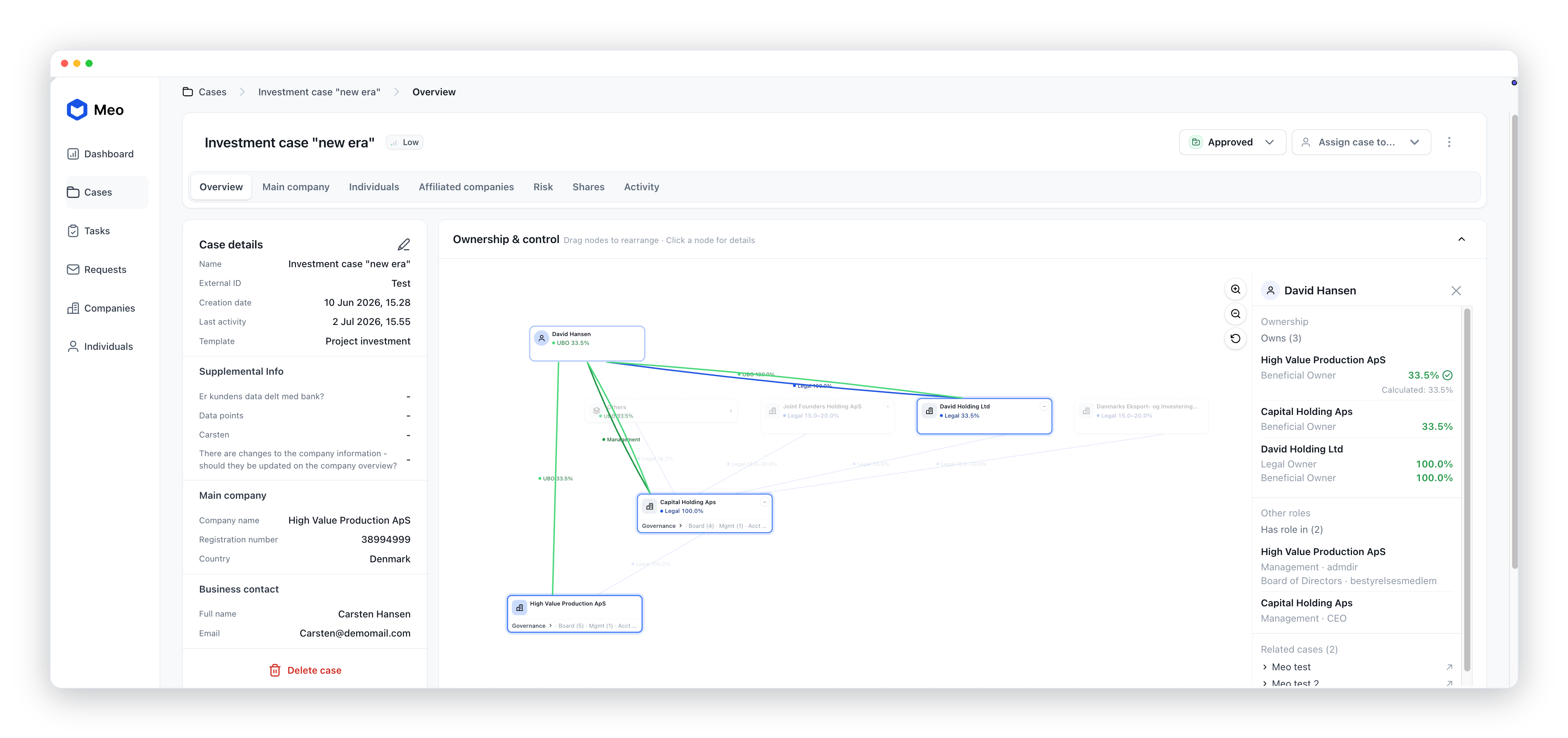

Case-based compliance, built for the AMLR

- Individual risk assessment per case

Every case and transaction is scored against its own risk profile - the case-based approach the AMLR's risk-based framework requires. - All compliance tasks in one queue

Document approvals, screening reviews and data-update requests tracked with clear ownership. - Alerts from official sources

Notifications when company registries or screening lists change, feeding your ongoing-monitoring duty directly into the task list. - A defensible audit trail

Statuses, decisions and assignments logged per case - evidence ready when the supervisor asks.

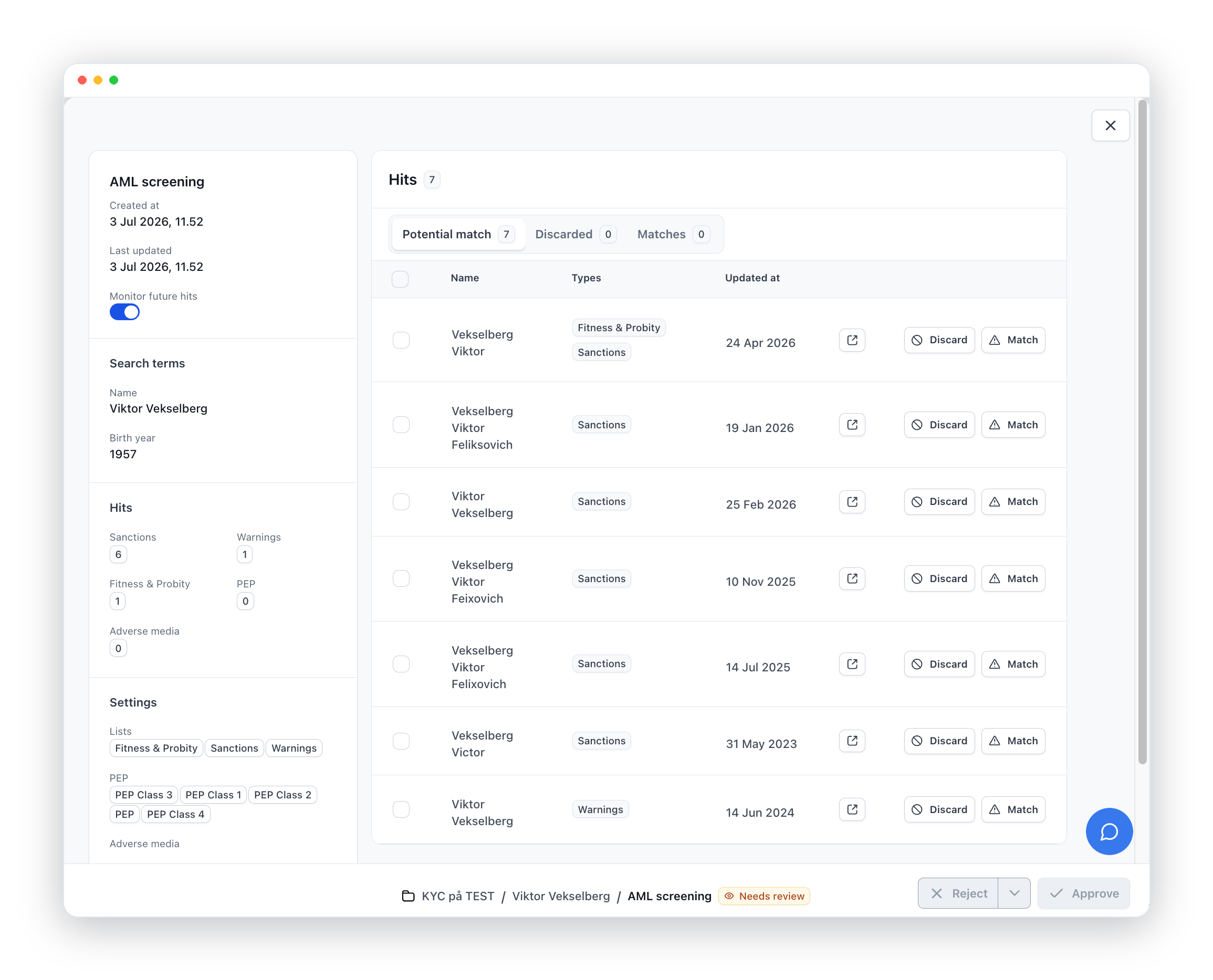

AML screening that never stops

- Individuals and companies

Screen natural persons and legal entities alike, with fuzzy matching that catches spelling variants and name forms. - Alerts on new hits

When a client appears on a list tomorrow, you know tomorrow - not at the next annual review. - Structured hit handling

Potential matches are reviewed, matched or discarded with a documented decision on each - no hit left unresolved. - Monitoring as the AMLR requires

Ongoing monitoring of the business relationship - the AMLR's standing requirement, running by default.

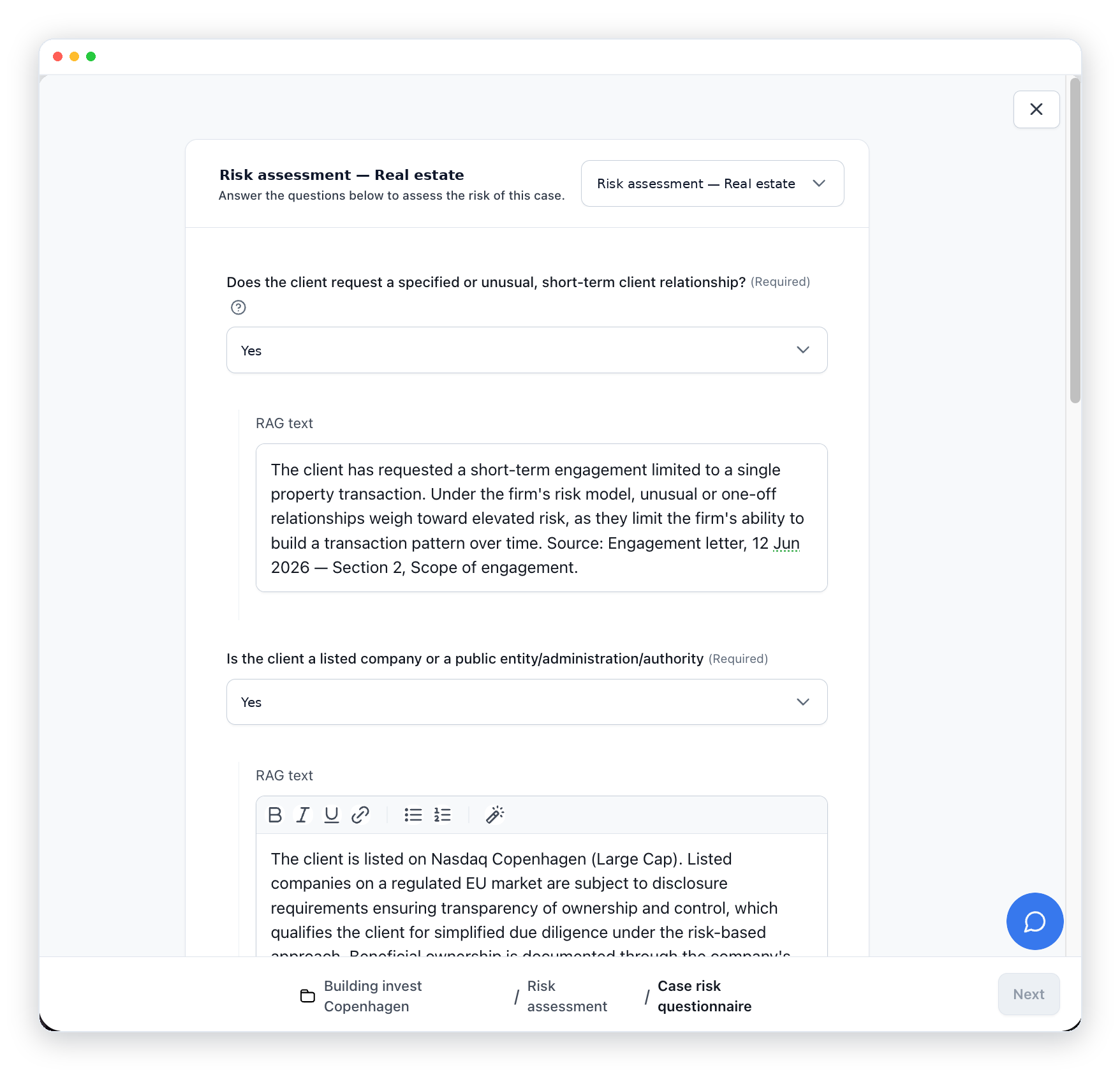

RAG Intelligence

- Answers with sources, not guesses

Every AI-assisted answer is retrieved from your verified case data and cited to the document it came from. Retrieved, not generated. - Grounded in your own data

The AI reads the client file, the engagement letter, the registry extract — and writes from those sources alone. - Supportive, never autonomous

RAG Intelligence drafts and documents; your compliance officer decides. Built for GDPR Article 22 and the EU AI Act. - Audit-ready by design

Each answer carries its source reference, so any assessment can be traced back years later.

Start at 90%, not zero

Of regulatory experience

Ready from day one

Built for the AMLR

AMLR - templates built for your sector

Meo powers industry giants’ compliance excellence

Case studies

Get access to trusted providers

Our blog

RAG Intelligence

Compliance work cannot tolerate invented answers. This paper introduces RAG Intelligence — a category of compliance technology built for one purpose: to make AI defensible in the contexts where defensibility is the entire point.

Executive summary

Compliance work cannot tolerate invented answers. Yet the dominant model for AI today, generative AI, is built to produce plausible-sounding output, not provably-sourced output. For any regulated work, this is not a limitation that can be patched with better prompting. It is an architectural mismatch.

This paper introduces RAG Intelligence: a category of compliance technology in which every output is retrieved from verified source material, cited to its origin, and never generated from a model's internal parameters. It is built for one purpose — to make AI defensible in the contexts where defensibility is the entire point.

RAG Intelligence is not autonomous. It does not make decisions, file reports, or replace the responsibility of the compliance officer. It does the part of compliance work that software can do well — retrieving the right document, surfacing the relevant data, paragraph, or business procedure, drafting a sourced summary — and leaves every decision in the hands of a human.

For any EU regulated firm preparing for the AI Act (Regulation (EU) 2024/1689, mostly applicable from 2 August 2026), RAG Intelligence is the standard that lets you adopt AI without exposing the firm to the risks that have made compliance teams rightly sceptical of it.

The problem with generative AI in compliance

Generative AI systems produce answers by predicting what text should come next. They draw on patterns learned during training, not on verifiable source material. When they are right, they are useful. When they are wrong, they are confidently, fluently, and convincingly wrong.

For most use cases this trade-off is acceptable. For compliance work, it is not — and under any plausible regulatory future, it will not be.

A compliance officer reviewing a customer file is not looking for plausible answers. They are assembling a defensible record. Every conclusion — this customer is low-risk, this beneficial owner is identified, this transaction does not require a Suspicious Activity Report (SAR) — must be traceable to a source the firm can produce on demand, years later, to a regulator, an auditor, or a court. This applies for any compliance work under any legal framework.

Generative AI breaks this requirement in three ways:

It cannot show its work

The output of a generative model is not derived from a specific document; it is synthesised from statistical patterns across an entire training corpus. There is no citation to produce, no audit trail to follow, no way to answer the only question that matters in a regulatory review: where did this come from?

It invents what it does not know

Generative models do not distinguish between facts they have seen and facts that are merely consistent with what they have seen. Faced with a customer who resembles other customers in the training data — but is not them — the model fills in the gaps from pattern, not from the file in front of it. A beneficial owner is named who does not actually own the company. An ownership structure is described that resembles other structures the model has seen but is not the one on the customer's documents. A risk profile is asserted that no document in the file supports. The output looks the same whether it is correct or fabricated. For a recipe, this is acceptable. For compliance, fabrication is not a quality problem — it is a liability event.

It cannot be governed at the output layer

Because generative output is a product of the model's internal weights, the firm cannot constrain what the model can say to what the firm has actually verified. The model's universe of possible answers is whatever it was trained on, much of which the firm does not control, did not approve, and cannot audit.

These are not edge cases. They are how generative AI works. No amount of prompt engineering changes the underlying architecture.

The autonomous-agent problem

The direction enterprise AI is moving makes this worse, not better. The most actively-marketed category in 2026 is agentic AI — systems designed to take actions, make decisions, and execute workflows with minimal human oversight. A specific sub-category has emerged in regulated industries: AI compliance agents, marketed as autonomous or semi-autonomous systems that take over the collection of data, the reviews, risk assessments, and onboarding decisions on the firm's behalf.

For most domains, autonomy is a reasonable productivity goal. For compliance, it is the opposite of what the regulation requires.

National legislation across the EU — and equivalent regimes in the UK, the US, and other jurisdictions — places the obligation to assess, decide, and report on a named human: the firm's designated compliance officer. The incoming AMLR and AMLD6, applying from 10 July 2027, are a good example: they harmonise these obligations across the EU and increase the standards for documented, defensible decision-making, supervised by the new EU Anti-Money Laundering Authority (AMLA). The EU AI Act explicitly classifies certain compliance and risk-scoring applications as high-risk, with mandatory human oversight requirements. GDPR Article 22 restricts solely automated decision-making that produces legal or similarly significant effects on individuals.

An AI system that approves customers, assigns risk classifications, or files reports on its own is not a productivity tool. It is a regulatory exposure — and the AI compliance agent category, at least where it takes autonomous action on decisions the regulation reserves for a human, is exactly that exposure dressed as innovation.

This is the trap that has made compliance teams across regulated industries wary of AI adoption: the louder the AI is marketed, the less it looks like something the firm's designated compliance officer can sign their name to.

What RAG Intelligence is

RAG Intelligence is the application of Retrieval-Augmented Generation — a well-established technical pattern in AI — to the specific demands of regulated work.

In a RAG system, every output is constructed in two steps. First, the system retrieves the relevant source material from a controlled knowledge base — the firm's own customer files, the applicable legislation, supervisory guidance, the firm's internal policies. Second, the language model is constrained to produce output only on the basis of what was retrieved, with citations back to the source.

RAG Intelligence is the discipline of doing this correctly for compliance work. That means three architectural commitments that go beyond generic RAG:

Retrieval is the source of truth, not a hint

Many RAG implementations use retrieval as one input among others, blending retrieved content with the model's parametric knowledge. RAG Intelligence does not. If the retrieved sources do not contain the answer, the system says so. It does not fill in the gap from the model's training data.

Every output is cited

Not summarised with a footnote — cited at the level of the specific source, the specific document, and where possible the specific passage. A compliance officer reading a RAG Intelligence output can verify every claim against the source it came from.

The system never decides

RAG Intelligence retrieves, surfaces, summarises, and drafts. It does not approve customers, assign risk scores, file reports, or take any action that the regulation reserves for a human. Decisions are made by the firm's designated compliance officer. RAG Intelligence assembles the basis on which they decide.

The shorthand is: retrieved, not generated. Supportive, not autonomous. Cited, not summarised.

Why this matters for regulated professional services

For any firm operating under specific legal obligations and preparing for the EU AI Act's high-risk requirements, the question of AI adoption is not whether AI can help with compliance. The benefits — faster onboarding, more consistent risk assessment, easier document review — are obvious. The question is whether the firm can adopt AI without taking on a new category of risk in the process.

RAG Intelligence is designed around this question. Five properties make it fit for purpose.

Defensibility

Every output produced by a RAG Intelligence system can be defended in front of a regulator, an auditor, or a court, because every output is grounded in a source the firm controls and can produce. There should be no hallucination to explain, no model behaviour to defend, no black box to apologise for. There is only the source, and what was retrieved from it.

Regulatory alignment

Because RAG Intelligence is decision-support rather than decision-making, it is designed to sit outside the EU AI Act's high-risk categorisation for autonomous decision systems, and outside GDPR Article 22's restrictions on solely automated decisions. It belongs to the same regulatory category as the calculators, search tools, and document templates the firm already uses — a tool the compliance professional applies, not an actor the firm has to govern.

Data sovereignty

A correctly-built RAG Intelligence system runs on EU-based infrastructure with self-hosted language models inside the EU. No customer data leaves the EU. No third-party model provider sees a single customer file. The firm's data stays the firm's data.

Auditability

Every retrieval, every query, every output, every citation can be logged. The firm has, on demand, a full record of what the AI was asked, what it retrieved, and what it produced. This is what an internal control system looks like. It is also what makes ISAE 3000 and ISO 27001 assurance possible over AI workflows — something generative AI, by its nature, makes far harder.

Human authority

The compliance officer remains the compliance officer. They review what the system surfaces, they confirm what the system drafts, they make the call. The system reduces the time they spend on retrieval and assembly. It does not reduce the time they spend on judgement, and it does not pretend to.

Workflow automation is not enough

The compliance technology market has, until now, been defined by workflow automation. Existing platforms collect documents, route them through approval flows, schedule reassessments, and produce audit logs. They make compliance work faster. They do not make it more intelligent.

Workflow automation answers the question did the firm collect the right documentation? It does not answer does the documentation actually support the conclusion? That is the question regulators, auditors, and supervisors will increasingly ask.

RAG Intelligence is the layer above workflow automation. It does not replace the workflow — clients still need to be onboarded, documents still need to be collected, reassessments still need to be scheduled. But it adds something workflow automation cannot: every conclusion in the file, drawn from the actual source material in the file, cited to the page it came from. The compliance officer reviewing the assessment is not reading a summary the system invented. They are reading what the documentation actually says, organised for a decision.

Workflow automation gets the documentation collected. RAG Intelligence makes sure the documentation answers the question.

What RAG Intelligence is not

Defining a category is partly a matter of saying what falls inside it and partly a matter of saying what does not. RAG Intelligence is a precise term. It excludes several things that are sometimes marketed adjacent to it.

It is not generative AI with retrieval bolted on

A generative system that also searches the web or also consults a vector store is not RAG Intelligence if it still falls back on parametric knowledge when retrieval is thin. The discipline of RAG Intelligence is that retrieval is the floor, not a feature.

It is not agentic AI

A system that takes actions, makes decisions, or executes workflows autonomously is not RAG Intelligence, regardless of how well it cites its sources. RAG Intelligence is bounded by design: it informs the human, it does not act on the human's behalf.

It is not a chatbot

A conversational interface is a delivery mechanism. RAG Intelligence is an architectural standard. A chat experience built on RAG Intelligence is fine; a chat experience that calls itself RAG-powered while generating uncited summaries is not.

It is not a compliance decision system

RAG Intelligence does not assess risk levels, classify customers, or determine whether a Suspicious Activity Report is warranted. It surfaces the inputs to those decisions. The decisions belong to the firm's designated compliance officer.

The distinction matters because the regulatory and reputational risk profile of compliance AI depends entirely on which side of these lines a system sits on. RAG Intelligence is the side a regulated firm can actually adopt.

A standard, not a product

RAG Intelligence is not a Meo feature. It is a category — a standard that any compliance technology can meet or fail to meet. A platform delivers RAG Intelligence if, and only if:

- All outputs are derived from retrieved source material in the firm's controlled knowledge base.

- Every output is cited to its specific source at a level of granularity that supports independent verification.

- The system does not produce ungrounded inferences when retrieval returns insufficient material — it reports the gap.

- The system does not make compliance decisions, take regulated actions, or operate autonomously on the firm's behalf.

- Every query and output is logged in a manner that supports audit and regulatory review.

A platform that meets these five criteria delivers RAG Intelligence. One that does not, does not — regardless of how it is marketed.

We publish this definition because the category needs one. As AI adoption in compliance accelerates, firms will be asked to evaluate a growing number of tools claiming to be safe for regulated work. Is it RAG Intelligence? is the question that cuts through the marketing and points at the architecture.

What this means for the next decade of compliance

The regulated firms that thrive in the next ten years will be the ones that adopt AI without abandoning the standards that make regulated professional work worth paying for: defensibility, traceability, and accountable human judgement.

This is not a contradiction. The wrong AI threatens those standards. The right AI reinforces them — by automating the parts of compliance work that should be automated, while leaving the parts that should not be exactly where they belong.

The window in which firms can choose their architecture rather than have it chosen for them is narrowing. The AI Act's high-risk classifications come into force across 2026 and 2027. Firms that adopt the wrong AI architecture now will spend the second half of the decade unwinding it.

RAG Intelligence is our name for the right architecture. We did not invent retrieval-augmented generation. We did not invent the regulatory principles it serves. We are naming the discipline of bringing the two together correctly, and committing — publicly, in writing — to the architectural standards that make it real.

If you are a compliance officer, a managing partner, or a procurement lead at a regulated firm, the question to ask of any AI tool entering your firm is no longer does it use AI? The answer is yes; it always will be. The question is now: is it RAG Intelligence?

If the answer is no, the firm will eventually be asked to explain why.

About Meo

Meo is a compliance platform for regulated industries. Founded in Copenhagen and built around the ability to evidence compliance, it covers the full workflow from initial risk assessment, to data exchange, to ongoing data management and audit-ready documentation. These are the activities at the core of regulatory frameworks spanning financial crime prevention, data protection, information security, and sector-specific obligations.

Meo ApS — RAG Intelligence for Compliance.

Always retrieved. Never generated.

.png)

Safeguarding law firms’ reputation with KYC/AML compliance

TLDR;

- Law firms face significant reputational risks from KYC/AML non-compliance, including client loss, damaged standing, and financial burdens, with only 30% of firms fully compliant in recent SRA inspections.

- Strong compliance can be a competitive advantage, attracting clients and talent while protecting and enhancing a firm's reputation.

- Proactive measures, such as user-friendly technology adoption, staff training, and transparent client communication, are crucial as rebuilding a damaged reputation is costly and time-consuming.

Law firms face significant reputational risks when failing to meet KYC and AML regulations.These risks extend beyond regulatory fines, potentially causing long-lasting damage to a firm's standing in the legal community and with clients.Its not unheard of a firm losing several key clients after news breaks of their AML compliance failures - even if the issues are quickly addressed (hint: we could be biased, but modern compliance software can help prevent such failures by automating checks and flagging potential issues early!)

SRA findings and public perception

The Solicitors Regulation Authority (SRA) inspections between April 2022 and April 2023 revealed that only 30% of firms were fully compliant with AML obligations.

This statistic, now public knowledge, can erode trust in the legal sector.

When a law firm faces enforcement actions and large fines media coverage often follows.

This publicity can tarnish a firm's image, making it difficult to attract new clients and retain existing ones.

The public may view non-compliant firms as unethical or negligent, regardless of the specific circumstances.If a law firm finds itself the subject of a damaging exposé in a major newspaper after receiving a fine for AML breaches, it could very much lead to the loss of major corporate clients and such cases are well known. It’s a field day for its competitors and it often takes years to rebuild lost reputation… and revenue.

Client trust

The high percentage of ineffective client risk assessments raise questions about law firms' ability to protect their clients’ interests. Worst case scenario, this can lead to a loss of client trust, particularly in matters involving sensitive financial information. Clients may worry - what’s fully understandable - about the security of their data and the firm's ability to maintain confidentiality. A firm could lose a client after failing to adequately explain their risk assessment procedures, despite having no actual data breaches.

Professional standing within the legal community

Compliance failures can harm a firm's standing among peers. The legal community may view non-compliant firms as less professional or competent, potentially leading to fewer referrals and collaborations. This can have a long-term impact on a firm's growth and success. Being publicly reprimanded for KYC failures may cost a firm valuable referrals.

A damaged reputation can make it difficult to attract top talent. Legal professionals may be hesitant to join or remain with a firm known for these kind of issues, fearing association with unethical practices or a lack of professional development opportunities.

While direct fines are significant, the financial impact of reputational damage can be far greater.Lost business, increased marketing costs to rebuild trust, and potential civil litigation from affected clients can create substantial financial burdens.

Global reputation in a connected world

For firms operating internationally, compliance failures in one jurisdiction can have global repercussions. The interconnected nature of the legal world means that reputational damage can quickly spread across borders, affecting a firm's standing in multiple markets. A firm could see a significant decrease in new matter openings across their international offices after facing AML issues in just one location, despite clean compliance records elsewhere.

Centralised, technology-driven compliance systems could help maintain consistent standards across all offices.

Long-term recovery challenges

Rebuilding a damaged reputation takes time and resources. Firms may need to invest heavily in compliance improvements, public relations efforts, and client relationship management to regain trust. This process can divert resources from core legal work and growth initiatives.

It could take several years of focused efforts and substantial investment to return to their previous level of profitability and client trust following a major compliance scandal.

Positive reputation is a competitive advantage

Conversely, a strong reputation for compliance can become a valuable asset. Firms known for their rigorous KYC and AML practices will likely attract clients seeking trustworthy legal partners, particularly in high-risk or sensitive matters. This positive reputation can lead to business growth and build stronger client relationships. You could see an increase in high ticket corporate clients over time due to a well-publicised investment in advanced AML software. It can affect your bottom line in both ways.

Client education is important

Law firms can mitigate reputational risks by educating clients about their compliance efforts. Transparent communication about KYC and AML procedures can demonstrate a firm's commitment to ethical practices, potentially strengthening client trust and loyalty. For example, a firm could see a significant reduction in client pushback during onboarding after implementing a clear, legalese-free guide explaining their KYC processes. Modern client onboarding and platforms allowing them to access their data could facilitate this transparency, allowing clients to easily understand and engage with compliance procedures too.

Proactive reputation management

Implementing robust compliance systems and regularly auditing practices can help prevent reputational damage before it occurs. Firms that take a proactive approach to KYC and AML compliance are better positioned to maintain a positive public image and professional standing.A firm could pass an unexpected inspection with flying colours after deciding to hire a full-time compliance officer and conduct quarterly audits, helping their reputation in the process. Automated compliance monitoring could support these efforts by providing real-time insights and alerts.

Industry leadership opportunities

Firms that excel in compliance can position themselves as industry leaders. Speaking at conferences, publishing thought leadership pieces, and participating in regulatory discussions can enhance a firm's reputation and influence within the legal community. As we have seen many times, a firm could be invited to present at a major legal tech conference after implementing a new, high quality AML system, raising their profile in the industry as leading the way to technological advancement in this rather conservative environment.

Reputation resilience through culture

Creating a strong compliance culture within a firm can build reputation resilience. When all staff members understand and prioritise KYC and AML requirements, the risk of reputation-damaging incidents decreases. Implementing a firm-wide compliance training programme should result in a substantial reduction in minor AML infractions over time, strengthening their reputation for diligence.

Leveraging technology for reputation protection

Investing in advanced compliance technologies not only improves efficiency but can also enhance a firm's reputation. Clients may view firms using accessible, user-friendly compliance tools as more professional, and the firm itself as heavily invested into their customer relations.Firm’s easy and secure onboarding can impress clients with an efficient - but transparent and understandable process that meets regulatory requirements. These solutions allow firms to manage compliance without needing technical expertise, yet demonstrate commitment to both: rules and client service. Customers usually don't expect their legal advisors to be tech experts, and neither should the KYC platform providers.

Are you curious how Meo protects law firms’ reputation with efficient and secure all-in-one compliance platform? Our experts are always happy to talk, no strings attached.

Striking the balance between efficiency and thoroughness in risk-based KYC

The security checkpoint

Imagine, that instead of working in compliance, you’re overseeing security protocols at a large international airport.

Your team cannot scrutinise everybody equally. It’s simply too busy. Some passengers will only go through a scanner, and others get a more thorough check. Your staff is trained to know what to watch for. They know who needs more of their attention:

- a nervous businessman with a one-way ticket to a high risk country

- a tourist with unusually heavy suitcase

- a frequent flyer, whose travel plans suddenly change

Any disruption to common patterns is potentially a red flag. The tiered screening system, where everyone goes through a basic screening, but more resources are allocated to those flagged by risk indicators, allows for thorough security - while maintaining operational efficiency.

There’s no chaos.

In any AML- regulated industry, you’re facing an almost identical challenge: how to vet customers without bogging down operations. Everybody gets baseline checks, and then you start looking deeper:

- a small business suddenly transferring large sums internationally?

- a politician from a country known for corruption?

- a small business suddenly transferring large sums outside of the country?

- a long time customer whose transaction patterns change for seemingly no reason?

This part isn’t just about ticking off boxes anymore. You’re building a detailed picture of each customer, adjusting the level of scrutiny based on the risk they can potentially pose.

This is a dynamic process, and a customer who started off as a low-risk can climb the risk ladder as their behaviour changes.

Striking the balance between the efficiency and thoroughness is at the heart of risk-based KYC. Maintaining strong security requires managing your resources well and this approach allows you to allocate them where the risk level demands it.

The future of KYC is automated

Of course, compliance officers must be extremely adept at identifying potential financial risks, just as airport security are trained to spot suspicious behaviour. Robust systems and well trained staff are the backbone of the implementation of risk-based KYC.

But there’s one more thing that can play a significant role and greatly improve the efficiency of the process, where the challenge lies in being both thorough and efficient.

Technology.

What if the security at the airport had a super-intelligent assistant, that could process information about every single passenger in a blink of an eye?

That's essentially what automated KYC systems are doing for AML-regulated entities.

They’re compliance experts working continuously around the clock. They're analysing large amounts of data, cross-referencing information, and identifying potential risks much faster than any manual process.

When a new customer begins the onboarding process, the automated KYC system starts working. It's not just verifying basic information, but it’s searching databases, examining documents, and in some cases, analysing biometric data. It's creating a comprehensive profile of the customer in a matter of moments. The system doesn't stop after the initial check. It's monitoring for any changes in your customer's behaviour or circumstances that might increase their risk level.

It can verify identities, check against sanctions lists, and analyse transaction patterns in a fraction of the time it would take a human operator.

This speed can significantly reduce onboarding times and improve the customer experience.

Efficiency however doesn’t come at the cost of thoroughness.

Automated KYC systems use advanced algorithms to comprehensively assess the risk. Human reviewers - being human - might miss some very subtle risk indicators, that a system that’s analysing a wide range of data points won’t. The system can continually monitor customer behaviour, flagging changes that could indicate increased risk. This ongoing assessment ensures thoroughness isn't sacrificed for speed.

Refining the balance

Can the automation replace the human oversight then? Despite the leverage it gives to the compliance teams, it’s unlikely this would happen anytime soon.

What it most definitely can do, is to help allocate human resources more effectively. Low-risk cases can be processed quickly, freeing up compliance officers to focus their expertise on complex, high-risk cases that require the level of judgement that only comes with professional experience.

This approach, of a tiered system of due diligence, it’s similar to our airport security analogy: most customers, like most passengers, can pass through the basic process. When the system flags a potential risk, it triggers a more through review.

What is the key to maintain the balance between efficiency and thoroughness then?

Refinement.

- Risk assessment criteria need regular updating to reflect new threats and regulatory changes. The financial world is not static, and neither should be the rules that govern it.

- System performance requires constant monitoring. False positives and false negatives should be carefully analysed to improve accuracy. This feedback loop helps the system learn and adapt over time.

- Data quality must be maintained- any system can only be as good as the information it processes. Ensuring data accuracy and completeness is important for both efficiency and thoroughness.

- Staff training is crucial. The compliance team needs to stay updated on how to interpret and act on the information it provides.

- Also audits and reviews of the entire process help identify areas for improvement. This includes assessing how well the automated system integrates with human decision-making processes.

At the gate

Airports aim to keep passengers safe without causing excessive delays, and in the same way, compliance officers aim to prevent financial crime while providing smooth service to legitimate customers.

Advanced scanning technology at airports quickly processes most travellers, flagging only potential risks for closer inspection - AML-regulated companies can now use comparable smart systems to simplify and enhance customer onboarding and monitoring.

Both systems require ongoing refinement to remain effective.

The airport security has to constantly adapt to new risks - financial threats and regulations change, so the KYC process must also be fine-tuned.

This ongoing improvement and refinement is a balancing act between speed and thoroughness.

You’re reaching your departure gate after passing through security.

If the process was smooth, you're relaxed and on time.

This is the goal of efficient KYC - customers clearing checks swiftly can access financial services without stress.

However, just as airport security must catch real threats, KYC must thoroughly identify high-risk cases.

Automated KYC systems help strike this balance.

When done right, this balanced approach creates a financial system that's secure yet accessible - much like an airport that's safe but still gets you to your gate on time.